The Role of Trusts in Safeguarding Your Children’s Future

In today’s unpredictable world, safeguarding your children’s future is more important than ever.

For parents, setting up a trust can be a strategic move to manage and protect assets for the benefit of their children.

Trusts provide clarity, control, and protection, ensuring that the resources you’ve worked hard to accumulate are used wisely for your children’s education, lifestyle, and long-term needs.

If you’re concerned about misuse, external risks, or premature access to the inheritance, trusts are the way to go as well.

Understanding Trusts: What Are They?

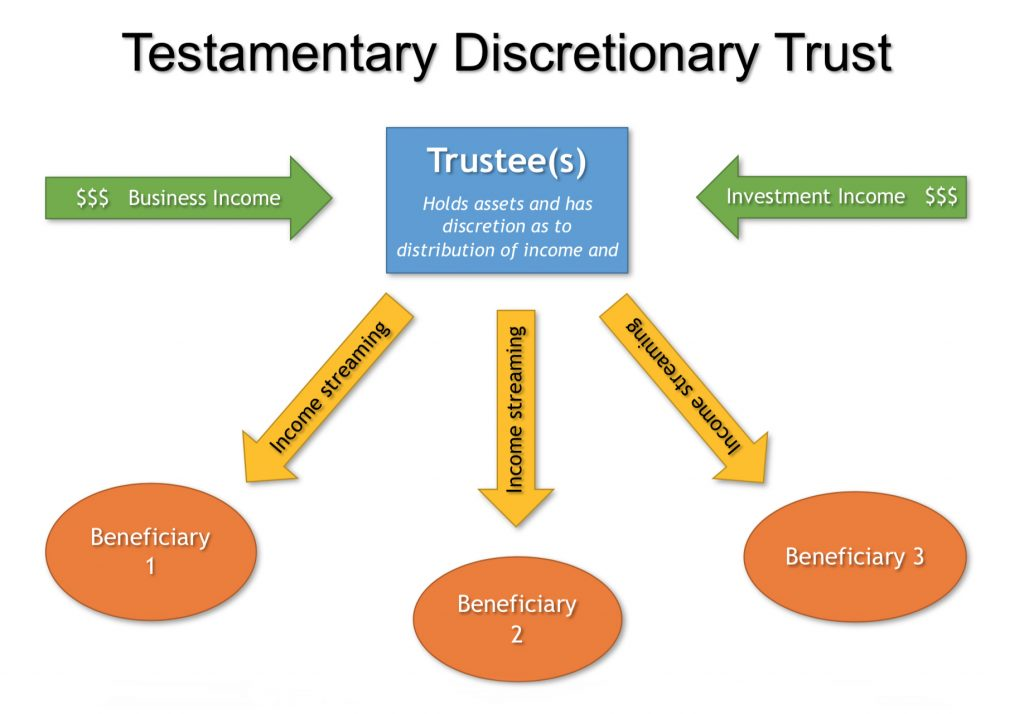

A trust is a legal arrangement where assets are held and managed by a trustee on behalf of your beneficiaries, such as your children.

You can set up different types of trusts based on your needs:

1️⃣ Living Trust

Created during your lifetime, allowing you to see its benefits in action.

2️⃣ Testamentary Trust

Established through your will and activated upon your passing.

3️⃣ Standby Trust

Set up now but activated only under specific circumstances like death or incapacity, without needing immediate funding.

The standby trust is particularly appealing for its flexibility and cost efficiency. It remains inactive until a triggering event, such as your death or incapacity, at which point it springs into action without having had to lock up assets prematurely.

Advantages include:

✅ Preparedness without immediate financial commitment.

✅ Peace of mind knowing the structure is ready when needed.

✅ Seamless transfer of life insurance proceeds, investment assets, or property into the trust.

✅ Avoids lump-sum distribution to minors at age 21.

✅ Option to appoint professional trustees to manage and distribute funds according to your instructions, protecting your assets from mismanagement or external claims.

How Trusts Support Your Children’s Education and Well-being

Trusts can be incredibly effective in managing funds for specific purposes like education and healthcare:

🎓 Dedicated Education Fund

Covers school fees, enrichment activities, and even overseas education expenses.

Payments are made directly, ensuring funds are used for their intended purpose.

🧒🏻 Care for Minors

Fills the legal void since minors cannot directly inherit assets.

Provides a structured way to release funds according to the child’s needs and milestones.

⭐ Support for Special Needs

Tailored to offer lifelong care, coordinating with entities like the Special Needs Trust Company (SNTC) for comprehensive support.

🪜 Staggered Payouts

Distributes assets at different life stages to foster responsibility and prevent financial imprudence.

🛡️ Protection from External Threats

Shields your children’s inheritance from creditors, divorce settlements, and other risks.

Local Legal Considerations

Trusts in Singapore are governed by robust legal frameworks, ensuring they operate smoothly and as intended:

- Governed by the Trustee Act and common law.

- CPF savings cannot be placed in a private trust, but CPF nominations can direct funds to named individuals.

- Insurance policies can be assigned to a trust (e.g. Section 73 policies)

- Trust companies or professional trustees are recommended for impartial and long-term management.

Steps to Establish a Trust

Here’s a step-by-step guide to help you navigate the process of establishing a trust or standby trust, ensuring that everything is tailored to your specific needs and legal requirements.

Step 1: Consult an Estate Planner or Trust Lawyer

The first step in establishing a trust is to consult with professionals who specialise in estate planning or trust law.

These experts provide valuable insights and guidance based on your unique financial situation, family dynamics, and long-term goals. They can explain the nuances between different types of trusts and help you understand which setup might best suit your needs.

| 💡Tips for Consultation Prepare Your QuestionsList questions about the trust process, costs, and what to expect. Gather Financial DocumentsBring details of your assets, including real estate, investments, and life insurance policies. Discuss Family NeedsTalk about any special considerations for family members, such as minors or dependents with special needs. |

Step 2: Decide on Key Elements of the Trust

The decisions you make about your trust are foundational to how it will operate. This step involves several important considerations:

Type of Trust

Choose between:

- A revocable trust, which allows you to make changes or revoke it entirely during your lifetime

- An irrevocable trust, which cannot be altered once it’s established

- A standby trust, which remains inactive until a specific event triggers its activation.

Trustee(s) and Guardian(s)

Selecting a reliable trustee is crucial, as this person or institution will manage the trust’s assets. Guardians are equally important if you have minor children; they will take care of the children’s daily and legal affairs if you are unable to do so.

Consider a professional trustee for impartiality and expertise, especially for complex estates. If choosing a family member or friend, ensure they are trustworthy and understand their responsibilities.

Conditions for Distribution

Define how and when the assets will be distributed to beneficiaries. You might set age-specific milestones, educational achievements, or other criteria that must be met before disbursement.

Step 3: Draft the Trust Deed

The trust deed is a legal document that outlines the trust’s terms and operation. Your estate planner or lawyer will draft this document, which includes:

Details of the Trustor/Settlor

That’s you, the person creating the trust.

Details of the Trustee

The individual or institution responsible for managing the trust.

Beneficiary Details

Those who will benefit from the trust.

Terms of Asset Management and Distribution

How the assets are to be managed and distributed, including any specific conditions or stipulations you’ve set.

Review Process

Carefully review the draft to ensure all details are correct and reflect your intentions.

Ask for clarifications on any legal terms or conditions that are unclear.

Step 4: Assign Assets

Finally, you will assign assets to the trust. This involves transferring ownership of your assets into the trust, which may include:

🏠 Real Estate

Deeds may need to be retitled into the name of the trust.

💰 Financial Accounts

Bank and investment accounts may need to be transferred.

💍 Personal Property

Items like art, jewelry, and other valuables.

For a standby trust, you’ll specify which assets will transfer into the trust upon activation, but you won’t transfer ownership until the specified event occurs (e.g., your incapacity or death).

Handling Assets

Work with financial institutions to ensure assets are properly transferred.

Remember to keep detailed records of all assets included in the trust for future reference!

Final Thoughts

Trusts, particularly standby trusts, offer a strategic and protective way for families in Singapore to plan for the future.

They complement other estate planning tools like wills, Lasting Power of Attorney (LPA), CPF nominations, and insurance, providing a holistic approach to family and financial planning.

Whether you have young children, special needs dependents, or a complex family situation, setting up a trust ensures that your legacy is managed according to your wishes, extending your care beyond your lifetime.

Reference

The views expressed in this media do not necessarily reflect the views of PFPFA Pte Ltd (“PFPFA”). The information provided herein is intended for general circulation and not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use will be contrary to local laws or regulation. You should also note that the information presented does not have regard to the specific investment objectives, financial situation or the particular needs of any specific individuals; and therefore, may not be appropriate to your individual needs. You should seek the advice of your financial adviser representative or a professional before making any commitment to purchase or invest in any investment product.

Estate planning services is provided by PFP Legacy Singapore, a sister company of PFPFA Pte Ltd. Estate planning and/or will-writing services are non-financial advisory services and thus are not regulated under the Financial Advisers Act.