In 2012, a tragic accident at Changi Airport took the life of a worker, leaving his widow, Madam Pusparani Mohan, and their four young children in debt. After her husband’s death, the family received nearly $1 million from insurance payouts and public donations, which could have provided financial security.1

Unfortunately, Madam Pusparani, having no experience managing such a large sum of money, struggled to make sound financial decisions for her family.

She used a portion to pay off debts, spent some on a family holiday to Genting Highlands, and invested $500,000 in her brother’s transport business, which eventually failed. By May of the following year, all the money was gone.2

Madam Pusparani’s story highlights how quickly money can slip away without proper financial and estate planning.

Receiving a windfall, whether from an inheritance, lottery, or insurance payout, can be overwhelming. In fact, it often brings more stress than stability. This is especially true if you're not used to handling a large sum.

These cases happen more often than we imagine. Many lottery winners end up losing everything, with almost a third declaring bankruptcy.3

A windfall can create a false sense of security; since the money is outside your regular income, it's easy to see it as "extra" or a "bonus". This mindset often leads to overspending or risky decisions, and before long, what seems like a blessing can become a burden.

So, when planning your wealth or estate, it's important to consider how well your beneficiary can manage a large sum of money.

Would it complicate things for them?

One of the key tools in wealth and estate planning is setting up a trust. A trust can provide your loved ones the support they need to make smart financial choices for their future. This ensures your assets truly benefit them in the long run.

In this article, we'll focus specifically on testamentary trusts and explore how they can help safeguard your legacy for your loved ones.

What is a Testamentary Trust?

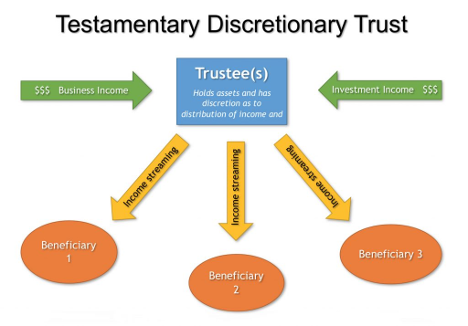

A testamentary trust is created through a Will that starts only after the person who made it (the Testator) passes on.

In a simple Will, your assets go straight to the beneficiary. With a Testamentary Trust, however, a Trustee manages those assets in accordance with your instructions.

As the Testator, you can choose a family member or a close friend as your Trustee. It can also be a corporate trustee or financial advisor, who has experience managing trusts. It all depends on how complex your estate is and who you trust to handle everything responsibly.

In Singapore, this kind of trust is useful for families with young children, dependents with special needs, or people who might not be able to manage a large amount of money well. Once set up, the trust is irrevocable upon the Testator’s passing.4

When your loved ones may not be financially savvy, setting up a testamentary trust can ensure their financial security, particularly when passing on large sums of money. It helps manage and protect your assets, ensuring they are used wisely and last longer.

Here's how setting up a testamentary trust can benefit your loved ones:

Structured Payouts

Instead of distributing the inheritance all at once, a trusted individual (the Trustee) could help arrange regular payouts from the testamentary trust to cover the living expenses of your loved ones.

This provides your loved ones with the financial means to handle daily needs without overwhelming them with a large sum. It also helps to make sure that the funds are used wisely.

Tailored Financial Advice

Managing an inheritance without experience can lead to costly mistakes.

A Trustee can guide better decision-making. With this support, your loved ones can sidestep risky investments or unnecessary expenses, focusing on preserving the savings for important needs and emergencies.

Ongoing Financial Support

For families who rely on a steady income, the sudden loss of a breadwinner can be devastating.

Subject to a mandate provided by the testator, a Trustee can invest the trust’s assets in ways that generate consistent income to support your family’s regular expenses. This helps make sure that the family’s needs are covered over time while protecting the capital from running out too quickly.

Preserving Inheritance

A testamentary trust can safeguard the inheritance for children until they are mature enough to manage it responsibly.

Instead of risking the loss of their future funds, the trust would keep the money safe. As the Testator, you can set specific conditions for accessing a larger portion of the funds, such as when a beneficiary reaches a certain age or milestones. This ensures that the fund is available for important milestones like education or buying a house.

Final thoughts

Simply leaving an inheritance doesn't guarantee a stable and comfortable life for our loved ones.

We must consider that not everyone is financially savvy. Without proper guidance, our beneficiaries may struggle to manage large sums over the long term.

However, you can help to make sure your absence doesn't become a burden by planning your wealth and estate effectively.

As we covered here, setting up a testamentary trust can be a helpful solution to provide long-term stability and protection for your loved ones after you pass on. This helps safeguard their financial future, even when they may not have the experience or knowledge to manage their finances.

Since different trusts serve different purposes, it is best to talk to an expert to find the best option for your situation.

Ultimately, your legacy is more than just wealth. It’s about the care you take in providing your loved ones with stability, peace of mind, and opportunity to thrive, even after you're gone.

We hope this article helped you in your investment journey. Share this with a friend who might need it too.

👋 Need additional advice and support on navigating your financial planning? Book a complimentary consultation with us.

Estate planning services are provided by PFP Legacy Singapore, a sister company of PFPFA Pte Ltd. Estate planning and/or will-writing services are non-financial advisory services and thus are not regulated under the Financial Advisers Act.

The views expressed in this media do not necessarily reflect the views of PFPFA Pte Ltd (“PFPFA”). The information provided herein is intended for general circulation and not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use will be contrary to local laws or regulation. You should also note that the information presented does not have regard to the specific investment objectives, financial situation or the particular needs of any specific individuals; and therefore, may not be appropriate to your individual needs. You should seek the advice of your financial adviser representative or a professional before making any commitment to purchase or invest in any investment product.

In Singapore, most of us grow up hearing the same advice: “Don’t worry, your CPF will take care of your retirement.” It’s comforting, but ultimately incomplete. CPF provides a strong foundation, but it was never designed to cover everything you’ll want or need in retirement. If you want more than “just enough”, like travel, freedom, […]

If you’re a parent of a child with special needs, you probably think about the future more than most. Questions like “Who will care for my child if something happens to me?” or “Will my child have enough financial support?” can feel overwhelming. Behind every worry is an opportunity to plan better. With the right […]

Many people breathe a sigh of relief once they’ve “ticked the box” of writing a Will. It’s a common assumption: if I have a Will, my wishes will be followed. Unfortunately, that’s not always the case. When a Will is drafted without the input of a trained estate planner — perhaps using a template-based online platform […]