Borrowing money is a big decision. It requires careful thought and planning. Whether you're looking to fund a home down payment, cover medical expenses, or handle other financial needs, understanding your loan options and managing debt effectively is crucial.

Types of Loans in Singapore

Loans are a popular choice for Singaporeans when they need to borrow money. While you can borrow from family or use a pawnshop, getting a loan is often the most reliable and regulated option.

Here are some of the most common types of loans:

Personal loans

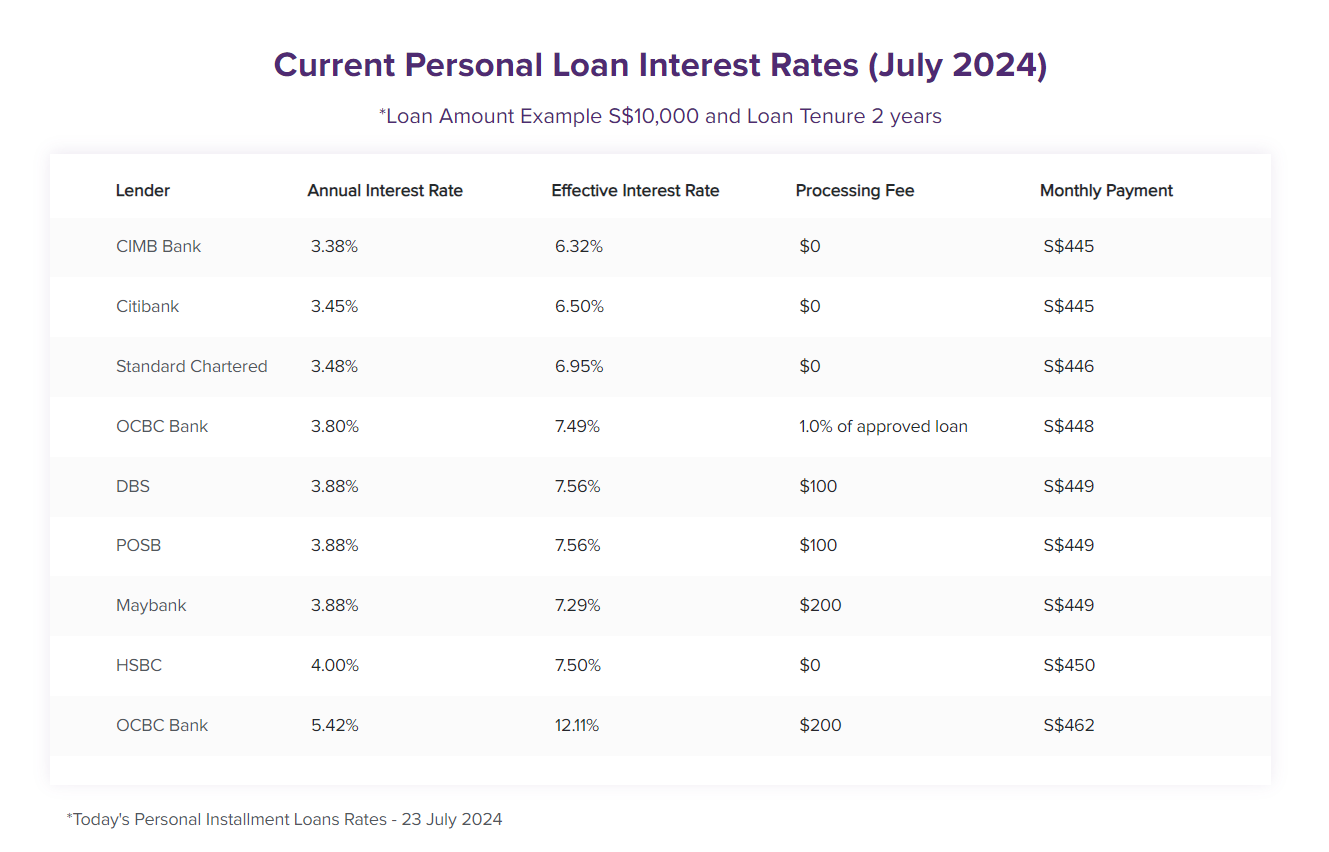

Personal loans are for private expenses, like paying off credit card debt or covering medical costs. These loans are usually unsecured, which means you will not have to offer anything as collateral.

The annual interest rates for personal loans in Singapore range from 3.38% to 5.42% per year, depending on your credit history.

Table 1: Personal loan rate comparison.Refer to footnote (1) for the source of this illustration.

Residential home loans

Using just your savings to buy a home can take years. If you're looking to settle down in Singapore, residential home loans can be a great help. These loans are for purchasing private or Housing and Development Board (HDB) properties.

There are two types of residential home loans you can take in Singapore. The first would be a private bank loan where floating interest rates are at 3.81%2.If you intend to purchase a HDB property, you can also apply for a HDB loan. The interest rate for a HDB loan is about 2.6%.3

Car loans

Car loans, or auto loans, are secured loans for purchasing new or used cars. Since car loans are secured, you need to provide something as collateral.

Businesses can leverage these loans to buy commercial vehicles, like lorries and vans.

The interest rates for car loans typically range from 2.48% to 2.98%, with slightly more complex terms.4

Education loans

Education loans are financial helping hands for students tackling university expenses such as tuition, hostel fees, and daily living costs.

DBS, OCBC, and UOB are some banks that offer education loans, each with its own set of terms.

The interest rates for these loans range from 4.38% to 4.78%.5

Credit Cards

A line of credit offers flexible borrowing up to a set limit, which you can reuse as you repay.

You can withdraw funds whenever necessary, making it a great choice for those who want easy access to advances.

The average interest rates for lines of credit range from 15% to 28%.6

Best Practices for Managing Debt

Managing debt can be tricky, especially if you're new to loans and budgeting. The last thing you want is to harm your credit score or miss payments.

However, when you handle debt responsibly, your loans can be a great way to ease your financial worries and set yourself up for success.

Here are some tips to help you stay on track:

Budget wisely

Creating a repayment plan is key to managing your debts better.

You can start with a detailed budget outlining your income, expenses and loan repayments. This helps you identify where you can tighten your budget and cut back.

When you keep track of your budget, there’s a higher possibility of you making payments on time and progressing towards your financial goals.

Use proven repayment methods

There are two main strategies for debt repayment: the snowball method and the avalanche method.

The snowball method focuses on paying off the smallest debt first to build momentum. It motivates you to keep up with your repayment as you see your debt shrink over time.

The avalanche method targets the highest interest-rate debt first. This strategy saves you more money on interest over time.

Choose a strategy that feels right for you and stick to it.

Cut back on extra expenses

A little goes a long way. Take a look at your daily expenses and identify where you can cut back on.

For instance, try cooking at home more often instead of eating out. It’s not only healthier but also saves a lot of money. Make a list when you go grocery shopping and stick to it to keep to your budget.

You can also think about those subscriptions and memberships you don’t use. Do you need that gym membership you never go to or those extra streaming services?

Making small changes to your lifestyle can free up money to pay off your debts faster.

Pay yourself first

To get a grip on your debt, prioritize debt payments by setting aside money for them before other expenses; "pay yourself first."

This way, your debts become a priority, not something you pay with what you’re left with.

To make this easier, automate payments to avoid missed deadlines and late fees. This way you avoid missed payments, late fees, and extra interest charges.

It also helps you spend within or below your means, giving you better control over your money.

Talk to a professional

If managing debt becomes overwhelming, it might be a good time to consult a financial advisor.

These experts will usually advise you according to your circumstances and guide you through creating a plan to get your finances back on track.

Sometimes, having someone experienced to cover your blind spots and provide clear, helpful advice is what you need to start feeling more in control of your money again.

Resist Temptation

Temptations are inevitable. So, anticipate and plan for your temptations. That’s the best way to manage them.

Research shows that one of the best ways to maintain self-control and stay motivated is by predicting and planning for temptations.

One idea is to use a cash-only system. Allocate cash in envelopes for different expenses to avoid overspending. This will make spending more tangible, adding a sense of reality to your spending decisions.

Final Thoughts

Borrowing money can feel overwhelming, but with careful planning and a good understanding of your options, you can stay in control. Managing debt well is key to financial stability.

Start by creating a budget you can stick to and be mindful of your spending. If things get tough, don't hesitate to talk to a financial advisor. With some discipline and smart financial habits, you can handle your debt confidently and work towards a secure financial future.

Remember, you're not alone in this journey—many people have successfully navigated debt, and you can too.

We hope this article helped you in your investment journey. Share this with a friend who might need it too.

👋 Need additional advice and support on navigating your financial planning? Book a complimentary consultation with us.

The views expressed in this media do not necessarily reflect the views of PFPFA Pte Ltd (“PFPFA”). The information provided herein is intended for general circulation and not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use will be contrary to local laws or regulation. You should also note that the information presented does not have regard to the specific investment objectives, financial situation or the particular needs of any specific individuals; and therefore, may not be appropriate to your individual needs. You should seek the advice of your financial adviser representative or a professional before making any commitment to purchase or invest in any investment product.

Many people breathe a sigh of relief once they’ve “ticked the box” of writing a Will. It’s a common assumption: if I have a Will, my wishes will be followed. Unfortunately, that’s not always the case. When a Will is drafted without the input of a trained estate planner — perhaps using a template-based online platform […]

Why Your Money Personality MattersYour financial choices aren’t just determined by the numbers in your account — they’re shaped by your habits, emotions, and even the stories you grew up with about money. Maybe your parents drilled the importance of saving into you. Maybe you saw money as a tool to enjoy life. Or maybe, talking about […]

No Kids, Double Income… So Retirement Should Be Easy — Right? That’s what many DINK (Dual Income, No Kids) couples assume. After all, you’ve got no school fees, no childcare bills, and more freedom. But here’s the truth: Having no kids doesn’t guarantee a smooth retirement. In fact, it brings a different set of challenges […]