In many Asian cultures, owning a home symbolises success and stability, while renting is sometimes viewed as “wasting money”, or even "unsuccessful."

In Singapore, the pressure to own a property is influencing major life decisions, such as marriage.1 With the rising property prices and external pressure, many are eager to take advantage of housing grants like the Enhanced CPF Housing Grant and the Family Grant, often without fully considering personal goals.

However, homeownership isn't the only option available. Renting offers flexibility and other benefits that might better suit certain lifestyles and long-term goals.

So, should you rent or buy?

In this article, we’ll explore the crucial questions to ask before deciding, followed by a quick overview of the key differences between both options.

5 Key Questions to Guide Your Property Decision

Did I Check The Price-to-Rent Ratio?

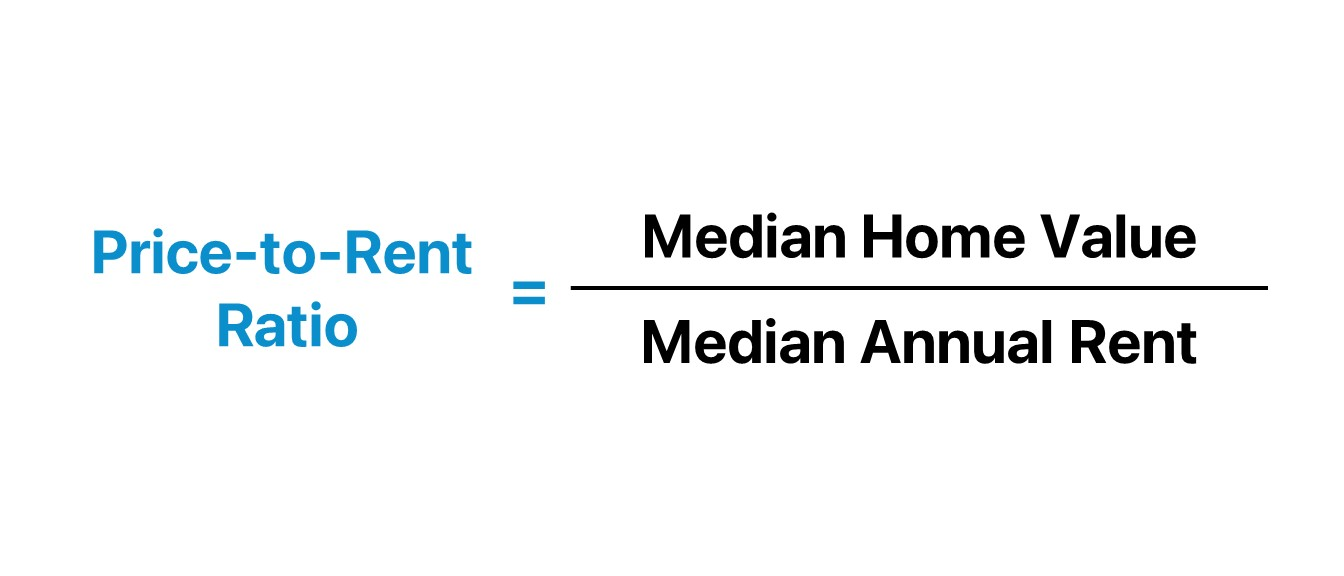

The price-to-rent ratio is a quick way to compare the cost of purchasing a home versus renting it, giving you a clearer picture of which option makes more sense for your financial situation.

The ratio tells you how many years of rent would equal the cost of buying the home.2

To calculate it, divide the median home value by the median annual rent.

For example, if a place costs $500,000 and the rent is $24,000 a year, you’d get a ratio of about 21. In this case, the ratio suggests that renting might be a smarter financial choice, as it would take 21 years of renting to equal the cost of buying.

Generally, if the ratio is under 15, buying could make more sense since it would take fewer years of renting to match the purchase price. However, if it’s over 20, renting might be the more financially sensible option, because it would take longer to break even through buying.2

How Stable Is My Income Currently?

Buying a home is a long-term financial commitment. So, understanding your income stability is key to determining if you’re truly ready for the responsibility– or if more planning is needed to reach that goal.

While buying a home can be incredibly rewarding, it often comes with unexpected costs. Beyond the initial down payment, there are ongoing expenses that can catch you off guard, like repairs, maintenance, and property taxes. Whether it’s a leaky roof or unexpected plumbing issues, these costs can be tough to handle if your income is inconsistent.

Having a steady and reliable income gives you the confidence to navigate these surprises without stress.

Renting, on the other hand, offers greater predictability, which can be a huge benefit if your income is less stable. With just a security deposit and the first month’s rent upfront, you know exactly what your monthly expenses will be. It makes budgeting simpler and more manageable. Plus, the landlord usually covers maintenance and major repairs, sparing you from the unexpected financial strain.

Do I See Myself Staying At One Location For At Least 5 Years?

In Singapore, the MOP (Minimum Occupation Period) requires HDB homeowners to live in their flats for at least five years before selling or renting out the entire space. You are also not able to purchase another property until the MOP period is over which is a minimum of 5 years.

So, if your plans are uncertain, fulfilling the MOP can feel restrictive and may limit your opportunities.

Renting offers flexibility, enabling you to move easily when life events occur, such as job relocations or changes in health needs. It saves you from the high costs and lengthy process of selling a property if you need to relocate.

However, if you're ready to settle down for at least 5 years, homeownership could be a great next step—allowing you to secure an asset under your name, build stability, and potentially grow your wealth over time.

How Important Is Homeownership To Me?

Homeownership is more than a financial decision, it's a lifestyle choice that will shape where and how you live, potentially for years. It's not a decision to be taken lightly just because "everyone is doing it".

If having a sense of stability and personal freedom matters to you, homeownership could be a meaningful investment. Owning a home gives you the freedom to decorate as you like, and create a space that truly feels like yours, offering a unique sense of belonging.

On the other hand, if flexibility is your priority, renting may be a better fit. Renting lets you adapt to life changes and explore new neighbourhoods without the long-term commitment of ownership. It’s perfect if you prefer to keep your options open.

What Role Does Property Play in My Financial and Personal Goals?

For many, a home is more than just a place to live. It is a chance to build long-term wealth and provide stability and security for future generations.

If building wealth and creating a family legacy through real estate aligns with your goals, buying a home can be a strategic investment. Every mortgage payment builds your ownership in an asset that could grow in value over time. Plus, it offers financial security and options for rental income if you decide to lease it out later.

But, real estate isn’t the only way to build and preserve wealth.

If your personal goals are more focused on flexibility, liquidity, or investing in other avenues, homeownership doesn't have to be a top priority. Renting keeps your capital accessible open, so you can diversify into other investment opportunities that align more closely with your goals.

Renting vs. Buying: A Quick Overview

Renting

Buying

Short-term commitment, typically 1 to 2 years3

Commitment

Long-term commitment, usually 25-30 years for a mortgage4

A minimal deposit, such as a 2-month upfront payment, might be required.

Upfront Costs

A significant downpayment is required, which can be partially covered CPF5

Monthly rental payments

Monthly payments

Monthly mortgage repayments based on loan tenure

More flexible, allowing you to move once the lease ends

Flexibility

Less flexible, as selling the property takes time, making relocation more challenging.

No property ownership

Ownership

Property becomes an asset once the mortgage is fully paid off

Few or no renovation options

Personalisation

Freedom to renovate and personalise the space

Lower financial commitment and risk

Financial commitment

Higher financial commitment with long-term debt

Carries the risk of rent increases or lease termination

Cost stability

Offers more predictable housing costs during the fixed-rate period of a mortgage

No wealth accumulation through renting

Wealth

Potential for wealth accumulation if the property value appreciates

Ideal for those with mobile careers

Career and lifestyle

Best for individuals who prefer stability

Suitable for short-term living arrangements

Living arrangements

Offers long-term stability and a sense of community

Influenced by rental market fluctuations

Market influence

Influenced by real estate market values and interest rates

Rented property cannot be inherited

Legacy

Property can be inherited by heirs

The Bottom Line

So, is renting or buying the better option in Singapore?

The answer largely depends on your personal goals, financial situation, and lifestyle. Your choice may differ from someone else’s based on these unique considerations.

For those planning to stay long-term and build wealth or a family legacy, buying a home might make more sense.

However, homeownership isn’t always the right choice for everyone.

You should not only consider the high costs of owning property in Singapore but also if the long-term financial commitment aligns with your goals. Renting can be a more practical option for those who value flexibility or are waiting for market conditions to improve.

Ultimately, the best decision is the one that fits your needs and circumstances.

We hope this article helped you in your financial journey. Share this with a friend who might need it too.

👋 Need additional advice and support on navigating your financial planning? Book a complimentary consultation with us.

The views expressed in this media do not necessarily reflect the views of PFPFA Pte Ltd (“PFPFA”). The information provided herein is intended for general circulation and not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use will be contrary to local laws or regulation. You should also note that the information presented does not have regard to the specific investment objectives, financial situation or the particular needs of any specific individuals; and therefore, may not be appropriate to your individual needs. You should seek the advice of your financial adviser representative or a professional before making any commitment to purchase or invest in any investment product.

If you’re a parent of a child with special needs, you probably think about the future more than most. Questions like “Who will care for my child if something happens to me?” or “Will my child have enough financial support?” can feel overwhelming. Behind every worry is an opportunity to plan better. With the right […]

Many people breathe a sigh of relief once they’ve “ticked the box” of writing a Will. It’s a common assumption: if I have a Will, my wishes will be followed. Unfortunately, that’s not always the case. When a Will is drafted without the input of a trained estate planner — perhaps using a template-based online platform […]

Why Your Money Personality MattersYour financial choices aren’t just determined by the numbers in your account — they’re shaped by your habits, emotions, and even the stories you grew up with about money. Maybe your parents drilled the importance of saving into you. Maybe you saw money as a tool to enjoy life. Or maybe, talking about […]